What is an Annuity?Annuities are contractually-executed, relatively low-risk investment products; the insured (usually, an individual) pays a life insurance company a lump-sum premium at the start of the contract. That money is to be paid back to the insured in fixed, incremental amounts, over some future time period (predetermined by the insured). The insurer invests the premium; the resulting profit/return on investment fund the payments received by the insured, and, compensate the insurer.

Conventional annuity contracts provide a predictable, guaranteed stream of future income (e.g., for retirement) until the death(s) of the beneficiaries(s) named in the contract, or, until a future termination date – whichever occurs first. These financial instruments have been used to accumulate funds and provide significant and sudden increases in personal income (via future, lump-sum withdrawals), all while legally avoiding the taxes (e.g., income-, capital gains-, estate-) that would otherwise be assessed on them. Immediate Annuities vs. Deferred AnnuitiesAn Immediate Annuity is an insurance policy which, in exchange for a sum of money, guarantees that the issuer will make a series of payments. These payments may be either level or increasing periodic payments for a fixed term of years or until the ending of a life or two lives, or even whichever is longer.

A Deferred Annuity is a contract that is chiefly a vehicle for accumulating savings with a view to eventually distribute them either in the manner of an immediate annuity or as a lump-sum payment Contact us to learn more about the right annuity for you. |

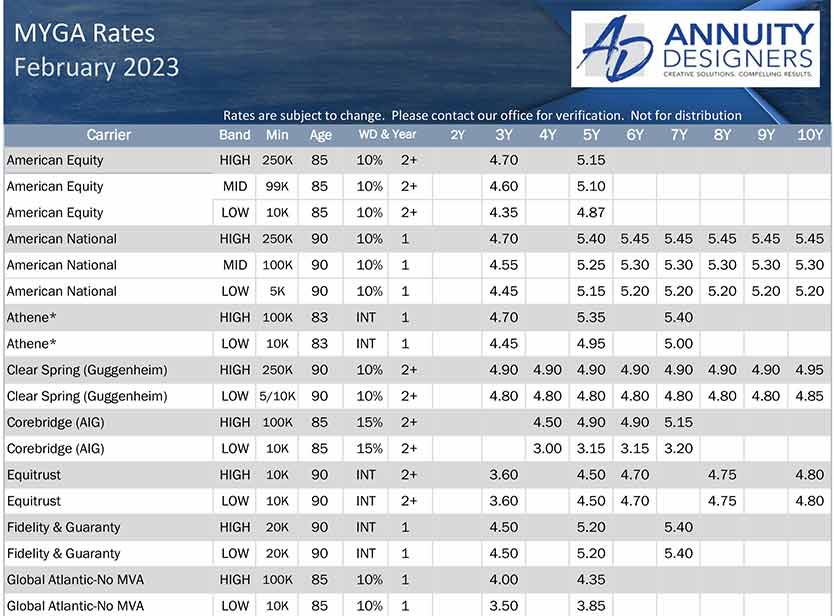

Annuities provide guaranteed income for life

|

We are licensed in Alabama, Georgia, Florida, Illinois, Indiana, North Carolina, Ohio, South Carolina, and Tennessee.

Navigation |

Connect With UsShare This Page |

Duluth Office:3675 Crestwood Pwky

Suite 400 Duluth, GA 30096 (864) 757-8140 |

Taylors Office:2801 Wade Hampton Blvd

Suite 301 Taylors, SC 29687 |